The modern American retirement system is currently undergoing its most significant overhaul in decades. Legislative efforts like the Secure Act and its successor, Secure 2.0, were sold as the ultimate fix for a nation facing a silver tsunami of aging workers with empty bank accounts. On paper, the plan is simple. By mandate and incentive, the government is forcing more employers to offer 401(k) plans and automatically enrolling employees who used to sit on the sidelines.

But the math does not hold up for the people who need it most. You might also find this similar article interesting: Why Trump is Right About Tech Power Bills but Wrong About Why.

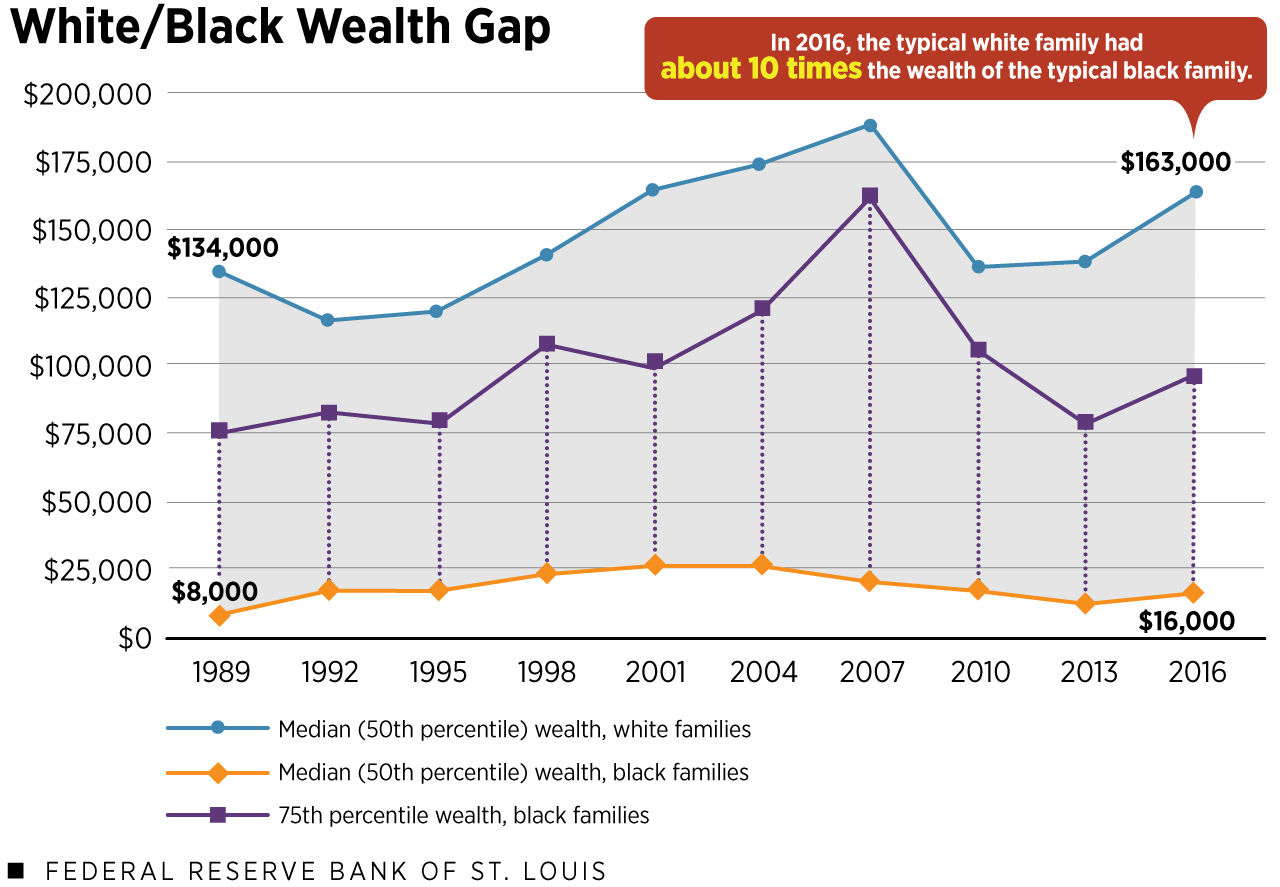

While these laws successfully expand the infrastructure of retirement savings, they do almost nothing to address the capacity to save. We are building a high-speed rail system for people who cannot afford the price of a ticket. For the bottom 50% of earners, the barriers to a dignified old age aren't just a lack of access to a corporate plan; they are rooted in stagnant wages, the rising cost of basic survival, and a tax incentive structure that perversely rewards those who already have plenty.

The Automatic Enrollment Illusion

The centerpiece of recent legislation is the push for automatic enrollment. The logic is that humans are lazy. If you sign them up for a 3% contribution by default, they will stay signed up. The data shows this works to increase participation rates. However, participation is not the same as preparation. As highlighted in recent coverage by The Wall Street Journal, the effects are significant.

Most automatic enrollment schemes start at a 3% contribution rate. For a worker earning $45,000 a year, that is roughly $1,350 annually. Even with a modest company match, that sum is a drop in the bucket compared to the projected costs of healthcare in retirement. By setting the "default" so low, the government has inadvertently created a "nudge" that leads to under-saving. Many employees assume that if the experts set the rate at 3%, then 3% must be enough. It isn't. It is a slow-motion disaster.

Furthermore, these mandates often exclude the most vulnerable sectors of the workforce. Small businesses with fewer than ten employees or those that have been in business for less than three years are frequently exempt. This leaves out millions of "gig" workers, contractors, and local service employees who form the backbone of the service economy. We are creating a two-tier society where white-collar workers are ushered into a subsidized future while the rest are told to figure it out on their own.

The Tax Code Favoritism

If you want to see where the real priorities of retirement legislation lie, look at the tax breaks. The 401(k) system is built on tax deferral. This means the higher your tax bracket, the more the government effectively pays you to save.

Consider two workers. One earns $200,000 a year and sits in a high tax bracket. When they put $20,000 into their retirement account, they see a massive immediate reduction in their tax bill. Now consider a worker earning $35,000. Their tax liability is already low. A tax deduction provides almost no tangible benefit to their daily life. They need that cash now for rent, groceries, and childcare.

The system is designed to accelerate the wealth of the affluent while offering crumbs to the working class. While Secure 2.0 attempted to remedy this with the "Saver’s Match"—a federal contribution for low-income savers—the implementation is buried in bureaucracy. It requires a level of financial literacy and tax-filing complexity that many of the intended recipients simply do not possess.

The Portability Trap

Another glaring hole in the current legislative framework is the issue of "leakage." When workers change jobs—which happens more frequently now than at any point in history—they are often faced with a choice: roll over their 401(k) or cash it out.

For a worker facing an immediate financial crunch, the temptation to take the cash and pay the 10% penalty is overwhelming. Current laws have made it slightly easier to move accounts, but they haven't solved the underlying problem of why people cash out in the first place. Without a "rainy day" fund, the retirement account becomes the only source of emergency liquidity. We are essentially asking the poor to pawn their future to survive the present.

The Myth of the Rational Saver

Economists love to talk about "rational actors," but real people have lives that are messy and unpredictable. The legislation assumes that if you give someone a tool, they will use it correctly. This ignores the reality of the "Sandwich Generation"—adults who are simultaneously supporting their own children and their aging parents.

When a parent needs a home health aide or a child needs college tuition, the 401(k) contribution is the first thing to be cut. No amount of "automatic" features can overcome a household budget that is consistently in the red. We have spent decades shifting the risk of retirement from the employer (via pensions) to the individual (via 401ks), and we are now seeing the limits of that shift.

The Pension Void

The death of the defined-benefit pension is the primary reason we are in this mess. In the mid-20th century, a worker could rely on a guaranteed monthly check for life. Today, that worker is an amateur investment manager. They are expected to understand asset allocation, expense ratios, and withdrawal rates.

The new legislation tries to fix this by allowing more annuities within 401(k) plans. The idea is to "create your own pension." But annuities are notoriously complex and often come with high fees that eat away at the principal. By opening the door for insurance companies to sell these products within employer-sponsored plans, the government may have just handed a golden ticket to the financial services industry at the expense of the American worker.

The Longevity Paradox

We are living longer, but we aren't necessarily living better. The "retirement age" is a moving target that fails to account for the physical reality of different types of labor. Raising the retirement age for Social Security might make sense for a lawyer or a programmer who works at a desk. It is a death sentence for a roofer, a nurse, or a warehouse picker whose body is broken by age 60.

Current legislation focuses on the accumulation phase—getting money into the accounts. It stays silent on the decumulation phase—how to make that money last for 30 years in an era of skyrocketing long-term care costs. A million-dollar nest egg sounds like a lot until you realize a private room in a nursing home can cost $100,000 a year.

The Missing Piece: Healthcare

You cannot talk about retirement without talking about the cost of staying alive. Medicare does not cover everything. It doesn't cover most long-term care. It doesn't cover dental or vision in many cases. The biggest threat to a senior's solvency isn't a stock market crash; it's a broken hip or a diagnosis of dementia.

By ignoring the intersection of healthcare and retirement savings, our current laws are merely putting a bandage on a gunshot wound. We are encouraging people to save for a future that will likely be swallowed whole by medical bills.

The Wealthy Get a Head Start

While the media focuses on how these laws help the "average Joe," the fine print often benefits the ultra-wealthy. Provisions that increase the age for Required Minimum Distributions (RMDs) allow those with massive IRA balances to keep their money growing tax-free for longer. This has nothing to do with helping a factory worker retire. It is a tool for generational wealth transfer.

If the goal was truly to solve the retirement crisis, the legislation would look very different. It would look like:

- Universal Portability: A single retirement account that follows you from your first job at a lemonade stand to your last day in the boardroom, regardless of employer.

- Mandatory Employer Contributions: Not just a match, but a requirement that companies put skin in the game for every hour worked.

- Reframing Social Security: Acknowledging that for the bottom third of earners, Social Security is not a "supplement"—it is the entire ballgame.

The harsh reality is that the 401(k) was never intended to be the primary retirement vehicle for the entire nation. It was a tax dodge for executives that accidentally became the national standard. We are trying to win a marathon using a pogo stick, and the legislation we are passing just gives the pogo stick a new coat of paint.

Until we address the fundamental disconnect between stagnant wages and the rising cost of living, we are just moving numbers around on a spreadsheet. The retirement crisis isn't a problem of "not enough people saving." It is a problem of "not enough people having anything left to save."

Check your last pay stub and look at the "Year to Date" contributions. If that number doesn't make you uncomfortable, you aren't paying attention to the math of the next thirty years. Determine your "burn rate" for basic survival today, then multiply it by 1.5 to account for healthcare inflation. That is the reality you are saving for, regardless of what the latest bill in Washington promises.